You need an Ozempic statistic that holds up, not a recycled number with no source. The verified 2026 figures: about 1 in 8 US adults (12%) are currently taking a GLP-1 drug, double the share from 18 months earlier (KFF, Nov 2025). Ozempic alone generated roughly $18 billion in 2025, tirzepatide (Mounjaro and Zepbound) reached $11.7 billion in a single quarter, and Eli Lilly overtook Novo Nordisk for the US GLP-1 lead.

Every figure on this page cites its primary source: Novo Nordisk and Eli Lilly earnings reports, KFF and RAND surveys, CDC data, IQVIA volume figures, and the FDA shortage database. Market caps and live figures are timestamped because they move daily.

We compiled the statistics across company revenue, prescription volume, US adoption, market share, projections, demographics, and supply. We update this resource quarterly, most recently in June 2026.

Get your custom peptide protocol:

- Tailored to your body and goals

- Precise dosing and cycle length

- Safe stacking combinations

- Backed by peer-reviewed studies

- Ready in under 2 minutes

Key Takeaways

The Ozempic and GLP-1 statistics cited most often from this resource:

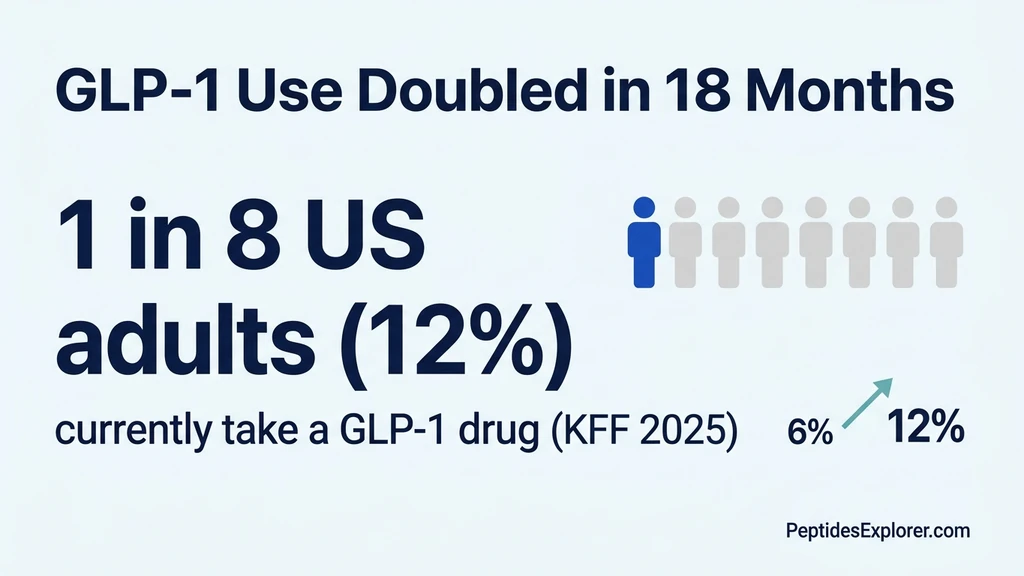

- 1 in 8 (12%): US adults currently taking a GLP-1 drug, double the 6% from 18 months earlier (KFF, Nov 2025)

- 18% of US adults: Have ever taken a GLP-1 (KFF, Nov 2025)

- ~$18 billion: Ozempic sales in 2025 (Novo Nordisk FY2025)

- ~$11.5 billion: Wegovy sales in 2025 (Novo Nordisk FY2025)

- $11.7 billion: Combined Mounjaro and Zepbound revenue in Q4 2025 alone (Eli Lilly)

- ~11 million: Unique US GLP-1 patients in Q2 2025 (IQVIA)

- Lilly overtook Novo: Eli Lilly took the US GLP-1 lead in 2025 (~57% share)

- Shortage over: FDA cleared semaglutide (Feb 2025) and tirzepatide (Dec 2024) from its shortage list

How Many Americans Take Ozempic or a GLP-1?

This is the single most-cited GLP-1 statistic, so it is worth getting exactly right.

About 12% of US adults, roughly 1 in 8, are currently taking a GLP-1 drug, according to a KFF Health Tracking Poll fielded in late 2025. A further 18%, nearly 1 in 5, have ever taken one. The poll surveyed 1,350 nationally representative adults.

| Measure | Rate | Source |

|---|---|---|

| Currently taking a GLP-1 | 12% | KFF, Nov 2025 |

| Ever taken a GLP-1 | 18% | KFF, Nov 2025 |

| Currently taking (18 months earlier) | 6% | KFF, May 2024 |

| Ever used a GLP-1 | 11.8% | RAND, Aug 2025 |

Current use doubled from 6% to 12% in about 18 months. One caution worth noting: the "current" and "ever" measures are different, and media sometimes mix them, so the RAND 11.8% (an "ever used" figure) should not be stacked on top of the KFF current-use number.

Who Uses GLP-1 Drugs

Adoption skews female and middle-aged, consistently across surveys.

| Demographic | Usage | Source |

|---|---|---|

| Women (ever used) | 22% | KFF, 2025 |

| Men (ever used) | 14% | KFF, 2025 |

| Adults 50-64 (ever used) | 30% | KFF, 2025 |

| Adults 50-64 (current) | 22% | KFF, 2025 |

Women are substantially more likely than men to have used a GLP-1, and the 50-64 age band leads every other group. An off-label user profile from Trilliant Health (patients without type 2 diabetes) skews younger, around 47.5 years on average, about 75% female, and over 90% commercially insured, though that single-firm figure is less authoritative than the KFF survey data.

Weight Loss vs Diabetes

The cultural image of Ozempic is a weight-loss drug, but the usage split is more balanced.

Among adults who have ever taken a GLP-1, about 61% used it to manage a chronic condition such as diabetes or heart disease, while roughly 38% used it solely for weight loss (KFF, 2025). The categories overlap, since a single patient can be both diabetic and overweight, so they do not sum to 100%. Among ever-users, 49% had a diabetes diagnosis and 77% had been diagnosed as overweight or obese in the prior five years.

Ozempic and GLP-1 Revenue

GLP-1 drugs are among the best-selling pharmaceuticals in history. The 2025 full-year figures come straight from company filings.

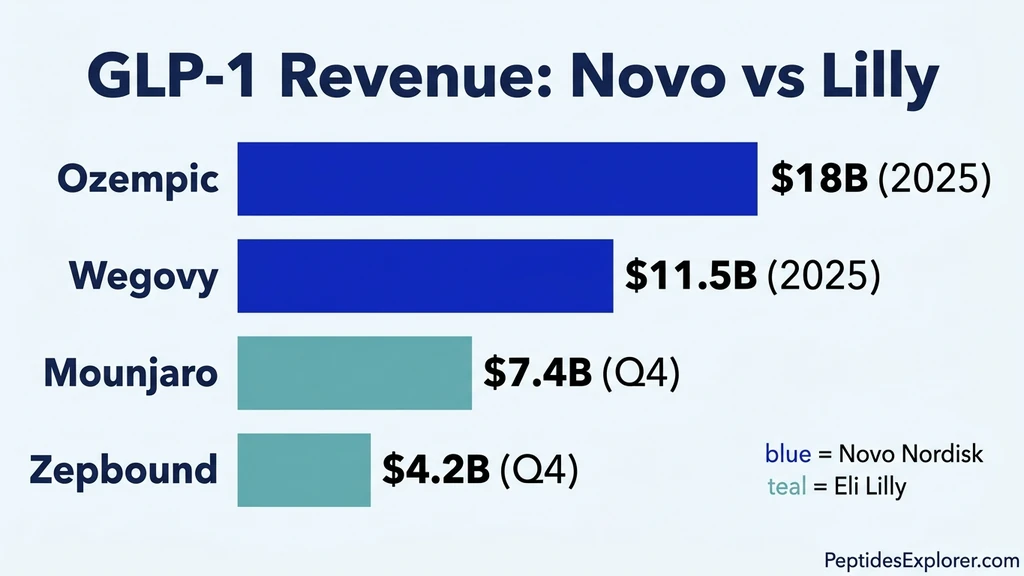

| Drug (Brand) | Company | 2025 Revenue | Note |

|---|---|---|---|

| Ozempic (semaglutide) | Novo Nordisk | DKK 127.1B (~$18.4B) | FY2025 |

| Wegovy (semaglutide) | Novo Nordisk | DKK 79.1B (~$11.5B) | FY2025 |

| Mounjaro (tirzepatide) | Eli Lilly | $7.4B in Q4 2025 alone | +110% YoY |

| Zepbound (tirzepatide) | Eli Lilly | $4.2B US in Q4 2025 alone | +122% YoY |

Sources: Novo Nordisk FY2025 report (Feb 2026); Eli Lilly Q4 2025 release (Feb 2026). Novo reports in Danish kroner; USD conversions are approximate at about 6.9 DKK per dollar.

Ozempic alone, at roughly $18 billion, out-earns the entire annual revenue of most large pharmaceutical companies. Eli Lilly's total 2025 revenue jumped 45% to $65.2 billion, driven overwhelmingly by its two tirzepatide brands. The combined Mounjaro and Zepbound quarterly run-rate of $11.7 billion shows how fast the tirzepatide franchise is scaling.

Lilly Overtook Novo

The competitive story of 2025 was Eli Lilly passing Novo Nordisk in the US.

Eli Lilly took roughly 57% of the US GLP-1 market in 2025, overtaking Novo Nordisk, with one Q4 2025 measure putting Lilly's US incretin share near 60%. Novo's own FY2025 report put its US total GLP-1 volume share at 44.8%. The exact percentage varies by metric (volume versus value, GLP-1 versus incretin), but the direction is unambiguous: Lilly leads and is extending it, powered by Zepbound.

Company scale tells the same story. Novo Nordisk briefly became Europe's most valuable public company in June 2025 at about $365 billion, then fell to roughly $200 billion by mid-2026 after trial setbacks. Eli Lilly's market cap sat near $1 trillion by mid-2026, roughly 5x Novo's. Market caps move daily, so treat those as snapshots, not fixed values.

Prescription Volume and Market Size

Volume data comes from IQVIA, the standard source for US prescription tracking.

There were about 11 million unique US GLP-1 patients in Q2 2025 across all indications (IQVIA). Combined semaglutide and tirzepatide prescription growth ran more than 500% year over year from late 2023 to mid-2025, though that growth figure comes from a secondary source citing IQVIA and should be treated as approximate.

Global market projections vary widely by firm and by how the market is defined, so they belong in a range rather than a single number.

| Projection | Value | Source |

|---|---|---|

| GLP-1 market by 2035 | ~$190B | Morgan Stanley |

| GLP-1 receptor agonists by 2034 | $254-257B | Fortune Business Insights / Polaris |

| GLP-1 analogues by 2034 | ~$323B | Polaris Market Research |

Analysts project the global GLP-1 market will reach roughly $130 billion to $320 billion by 2034-2035, depending on the firm and the definition. Morgan Stanley's ~$190 billion by 2035 carries the most editorial weight, but all market-research-firm projections are estimates built on proprietary methods.

Is There Still an Ozempic Shortage?

No. The multi-year GLP-1 shortage is officially over, which matters for anyone tracking compounded alternatives.

The FDA declared the tirzepatide shortage resolved on December 19, 2024, and the semaglutide shortage resolved on February 21, 2025. Neither drug is currently on the FDA shortage list. Because legal compounding depended on shortage status, the end of the shortage narrowed the basis for mass compounding, and enforcement discretion periods closed in 2025.

This is why 2026 looks different from 2023 and 2024 at the pharmacy: supply is stable, brand availability is consistent, and the compounding market has contracted. For what that means if you used a compounded version, see does compounded tirzepatide work.

Methodology

Every statistic on this page is sourced to one of the following, in descending order of weight:

- Company earnings reports (Novo Nordisk FY2025, Eli Lilly Q4 2025) for revenue

- Major surveys (KFF, RAND, CDC) for US adoption and demographics

- IQVIA for prescription and patient volume

- FDA shortage database for supply status

- Market-research firms (Morgan Stanley, Fortune Business Insights, Polaris) for projections, all marked as estimates

We lead with the most recent, most authoritative figure for each statistic. We do not stack "current use" and "ever used" survey measures, because they count different things. Market caps and share percentages are labeled with their date and metric, because they move and because definitions differ. Projection figures are presented as a range with the firm named, never as a single settled number.

Frequently Asked Questions

What percentage of Americans take Ozempic or a GLP-1 drug?

About 12% of US adults, roughly 1 in 8, are currently taking a GLP-1 drug, and 18% have ever taken one (KFF, November 2025). Current use doubled from 6% about 18 months earlier. This is the most-cited and most-recent adoption figure available.

How much money does Ozempic make per year?

Ozempic generated about DKK 127 billion, roughly $18 billion, in 2025 (Novo Nordisk FY2025 report). Its sister drug Wegovy added about $11.5 billion. Ozempic alone out-earns the total annual revenue of most large pharmaceutical companies.

Is Eli Lilly or Novo Nordisk bigger in the GLP-1 market?

Eli Lilly overtook Novo Nordisk for the US GLP-1 lead in 2025, holding roughly 57% share, driven by Zepbound and Mounjaro. By mid-2026 Lilly's market cap was near $1 trillion, about 5x Novo's. Novo's own report put its US GLP-1 volume share at 44.8%.

How many Americans are on a GLP-1 right now?

About 11 million unique US patients were on a GLP-1 in Q2 2025 across all indications (IQVIA). Survey data from KFF puts current adult use at 12%, or roughly 1 in 8. The two measures count differently (patient counts versus survey share) but both show massive scale.

How big will the GLP-1 market get?

Analysts project the global GLP-1 market will reach roughly $130 billion to $320 billion by 2034-2035, depending on the firm and how the market is defined. Morgan Stanley estimates about $190 billion by 2035. All such projections are commercial estimates, not settled figures.

Is there still an Ozempic or semaglutide shortage in 2026?

No. The FDA resolved the tirzepatide shortage in December 2024 and the semaglutide shortage in February 2025. Neither is currently on the shortage list. The end of the shortage also narrowed the legal basis for mass compounding of these drugs.

Who uses GLP-1 drugs the most?

Women are far more likely than men to use GLP-1s (22% versus 14% ever used), and adults aged 50-64 lead every age group at 30% ever used (KFF, 2025). Off-label weight-loss users skew younger and predominantly commercially insured.

Do most people take GLP-1 drugs for weight loss or diabetes?

Among adults who have ever taken a GLP-1, about 61% used it to manage a chronic condition such as diabetes or heart disease, and roughly 38% used it solely for weight loss (KFF, 2025). The groups overlap, since many patients are both diabetic and overweight.

The Bottom Line

The Ozempic numbers document a drug class that reshaped pharmaceuticals in a few years. About 1 in 8 US adults now take a GLP-1, Ozempic alone earns roughly $18 billion a year, and the tirzepatide franchise is scaling even faster, carrying Eli Lilly past Novo Nordisk for the US lead. The shortage that defined 2023 and 2024 is over.

Read the adoption figures carefully: current use and ever-used are different measures, and the market projections are estimates that span a wide range. The verified anchors, company earnings and major surveys, tell a clear story of scale.

Keep exploring the data:

- GLP-1 Side Effects Statistics: the trial numbers, separated from real-world data

- GLP-1 Cost Statistics: real prices, from list to self-pay to compounded

- Peptide Statistics 2026: 60+ verified facts across the industry

- Take our peptide quiz: a personalized protocol in 2 minutes

References

- 1.KFF (Nov 2025). Poll: 1 in 8 adults currently taking a GLP-1 drug. Link

- 2.Novo Nordisk (Feb 2026). FY2025 financial report. Link

- 3.Eli Lilly (Feb 2026). Q4 2025 financial results and 2026 guidance. Link

- 4.RAND (Aug 2025). Nearly 12% of Americans have used GLP-1s. Link

- 5.CDC/NCHS (Aug 2025). Data Brief No. 537, GLP-1 injectable use. Link

- 6.Morgan Stanley. GLP-1 weight-loss market may reach ~$190B by 2035. Link

*Educational content only. Not medical or investment advice. Market figures and company data reflect 2025-2026 reporting and change over time. Verify current figures with primary sources before relying on them.*

Helpful Tools

Related Articles

GLP-1 Side Effects Statistics (2026)

GLP-1 side effects by the numbers: 44% nausea on semaglutide, 4-7% quit in trials vs up to 64.8% within a year. Cited STEP/SURMOUNT trial data.

GLP-1 Cost Statistics 2026: Real Prices, Verified

How much GLP-1 drugs really cost in 2026: Wegovy lists at $1,349/mo but self-pay runs $349, Zepbound vials $299-449, compounded from $149. Verified prices.

Peptide Statistics 2026: 60+ Verified Facts

60+ peptide statistics for 2026: $52.6B market, 1 in 8 US adults on GLP-1s, search +652%, retatrutide 28.7% weight loss. Cited sources, updated quarterly.

FDA Peptide Crackdown 2026

Timeline of FDA actions against peptide vendors in 2025-2026. Why Peptide Sciences shut down, which peptides are banned, and what options remain.